Here’s my post on the big four U.S. banks: JPMorgan Chase, Citigroup, Wells Fargo, and Bank of America. I go over third quarter results and what’s happen for the big banks.

Reposted from Seeking Alpha. The full article is available here.

Preview:

Summary

- The big banks are hated. The negative sentiment creates an good entry point.

- Once dividends and buyback restrictions are lifted, the space could attract more investors.

- Q3 numbers suggest that banks are well-positioned to operate in an uncertain environment.

- If the economy improves and the banks can release some of the reserve set aside.

This is a brief article on the four main big U.S. banks and its recent results. Earnings season has come and gone for America’s biggest banks. The results were better than expected but the sentiment is still negative. There’s no love for banks and to be fair they are hard to love. The combination of ultra-low rates, the pandemic, a recession, credit issues, the election, and regulations is not the cocktail that attracts investors. The Feds has also announced that it was extending restrictions on share repurchases and dividends for the largest banks—those with more than $100 billion in assets—for at least one more quarter. Buybacks historically accounted for roughly 70% of the banks’ capital return to shareholders.

The shares of Bank of America (BAC), JPMorgan Chase (JPM), Citigroup (C) and Wells Fargo (WFC) fell after earning release. 2020 hasn’t been a good year for bank investments. The KBW Bank index (BKX) is down 30% year-to-date. To summarize, earnings have surprised to the upside as robust trading activity helped offset lower net-income margins, and profits weren’t crimped by having to add billions to reserves to protect against bad loans. But the problem with banks is often what you don’t see. Trust is important. Insurance companies and banks are often considered black boxes. You don’t know with certainty if you can trust the balance sheet. Accounting and disclosures are opaque. Deutsche Bank (DB) trades at a paltry 0.3 times book value. Accounting can conceal more than it reveals about economic reality. Do bank’s financial statements provide a meaningful clue about its risks?

Banks are integral to how our system functions. Bank results are akin to taking the pulse of the economy. You get a diagnosis on how things are doing. Without getting deeply technical on how a bank functions, they are one of the organs that decide how much money circulates in the economy. When consumers pay down loans, that money gets recycled into new loans. A healthy bank system is core to a healthy economy. Look at Europe. The old continent desperately needs its banks to function better. Despite its flaws, I fundamentally believe the U.S. banking system is the best in the world. They are excellent at their primary function of allocating capital to the most promising opportunities which leads to an overall increase in the standard of living.

I’m stating the obvious when I write that the pandemic has been hard on everyone. On the bank side, they got hit by a one-two punch.

The first punch, net interest income, which is the spread between interest earned on loans and interest paid to depositors, got squished as interest rate plunged. Borrowers paid down loans and hoarded cash. NII came under heavy pressure while provisioning improved.

The second punch is the uncertainty in the economy has caused banks to pull back on new lending, and increase the losses taken on existing loans. Also the new loans are made at lower rates which decrease future revenues.

I see banks as a long-term investment. They are slow moving and it takes forever to get through issues. A bad book of loans takes years to digest and regulatory issues also takes years to settle. That’s why on the short-term, it’s hard to invest in banks. I don’t think you will ever like what you see. But regulations are a necessary evil for banks. Regulations are there to prevent blow ups which are never good for anyone. Trust in the financial system is important to make sure things are running.

Despite the provisioning for loan loss and the effect of the pandemic, the bank balance sheets that have been tested for just about any outcome. They are solid. You probably heard of the new accounting standards, dubbed Current Expected Credit Losses, or CECL, are making those loan losses look even worse. CECL requires banks to book their anticipated losses upfront, rather than realizing them over the life of the loan. Banks have set aside billions for bad loans in case economic forecasts that are more dire than consensus views—cash that could be released if the situation improves. In this situation the accounting changes might provide a boost to the banks and their shares.

Despite the negative picture I just painted, I believe there are better days ahead for the banking industry.

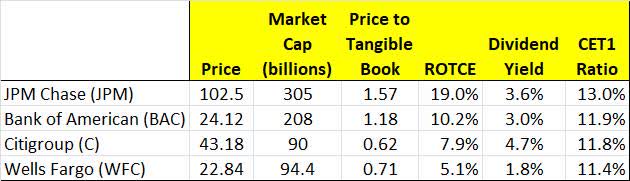

I wanted to do a brief overview of the four mains banks in the U.S. Here’s a table with some data. Of course, the metrics are just a starting point for further analysis. I used tangible book value as an anchor of valuation given that earnings are depressed by credit provisions.

Source: Data from filings

Source: Data from filings

[…] The Big Four (Brian Langis) […]