NTELOS Holdings Corp (NTLS) is my latest top idea on Seeking Alpha. It’s outside my traditional investing zone and its not for the faint of heart. NTLS offers a lot of upside but comes with risks and higher volatility. The daily price swings can be large. It has a speculative aspect to it. A lot of things can go right and a lot of things can go wrong. With that out of the way, here is part of the article:

Summary

- NTLS is trading at a 4.5x EV/EBITDA multiple. Current market peers are trading at a 7.8 EV/EBITDA.

- NTLS’s refocus on the Western market is good for the company. NTLS experienced strong growth in Q1 in its Western markets, its best for net adds since 2007.

- NTELOS is a potential takeover candidate. An offer could lead to gains upwards of 90%.

- NTELOS is in the process of completing its 4G/LTE network to be completed in early 2017. It should generate meaningful free cash flow thereafter.

- Agreement with Sprint extended to 2022. NTELOS will continue to be the exclusive network provider for Sprint services.

A quick glance at NTELOS Holding Corp. (NASDAQ:NTLS) looks messy and unappealing. NTELOS is a pure-play regional wireless carrier providing coverage to customers predominantly in West Virginia and western Virginia that has seen its stock price go straight to hell.

(click to enlarge)

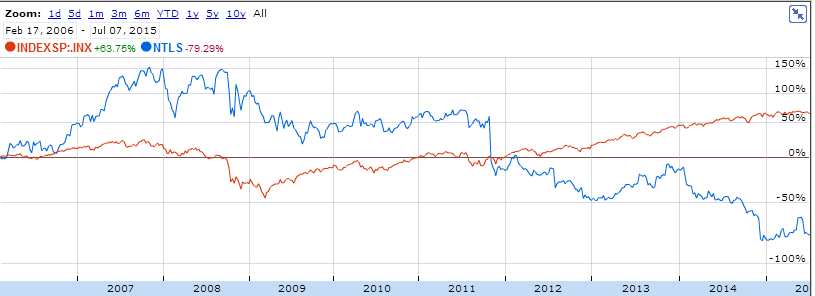

Source: Google Finance. NTLS vs. S&P 500. February 17, 2006 to July 7, 2015.

Investing in NTLS since inception would have been a disaster for investors. Since February 17, 2006, 80% of NTLS’s stock price melted away. You would have been better off investing in the S&P 500 with a ~63.75% return for the same period of time. Actually, a real return adjustment calculation is required because in late October 2011, NTLS split off Lumos Network (NASDAQ:LMOS) and you also need to account for the generous dividends NTLS distributed for a while. As of July 10, 2015, NTLS traded at $4.75, 30% above the 52-week low of 3.85 set on Jan 15, 2015, but it’s still down 60% over one year. NTLS has also underperformed its relative index up to December 31, 2014, and the price hasn’t changed much since:

(click to enlarge)

Source: NTELOS 2015 10-K

Among the factors behind NTELOS’s decline is the exit from the Eastern Markets, which represents about ~40% of its customers to focus on its Western Markets, which is more profitable. On top of that, add a high-debt load, intense competition, a CEO resigning, and the elimination of its dividend. Plus NTELOS was dropped from the S&P Small Cap 600 index, piling on the selling pressure.

The rapid adoption of smartphones, coupled with the prevailing unlimited data plans led to a massive growth in wireless data consumption, which subsequently caused high network congestion. Since then, carriers have made massive investments on their networks to optimize them for high data capacity. This was carried out through various measures such as acquiring more spectrum, increasing the number of cell towers, and upgrading of backhaul. It’s harder and harder to be a regional wireless operator. All this stuff is very expensive and the business is very much commoditized where it is difficult to differentiate yourself from your competitor (same phone, similar plans, comparable cost etc…).

You need a lot of financial muscle to roll out a project as capital intensive as the 4G/LTE network. Scale is essential in telecommunication. The large telecoms can take advantage of their superior scale and balance sheets to lay the groundwork for future growth. The smaller carriers are having a difficult time competing. Smaller regional players such as Cincinnati Bell (NYSE:CBB), Revol Wireless, Alltel, Clearwire, Centennial Wireless, Cox Communications, Dobson Communications, Golden State Cellular, MobiPCS have exited the industry. The industry is in consolidation. Softbank (OTCPK:SFTBY) acquired Sprint (NYSE:S), T-Mobile (NYSE:TMUS) bought MetroPCS, and AT&T (NYSE:T) purchased Leap Wireless (Cricket Communications).

So with such a rocky introduction you probably wonder where am I going with this?

The depressed value of NTELOS is hard to ignore, even with its high debt level it’s not all gloom and doom. The market’s perception is that NTELOS is a black hole and as a result the share price has sunk to a demoralized level. That’s the market for you and it works both ways. When it’s sunny everybody rushes to buy the stock and pumps up the stock price to an irrational level. And when it’s raining nobody wants to touch it. It’s has been raining for a while at NTELOS but there’s some nice weather forecast ahead.

The future of the business, the Western Markets, is both growing in revenues and subscribers. Just in Q1-2015 alone, subscriber base, now at 290,100, grew 5% over prior year benefiting from strong gross adds and a 30 bps reduction in churn. It’s on track to generate positive EBITDA in FY2015. One of the biggest headaches, the total debt of $524.2m, is under control. The debt matures in November 2019, and NTELOS only has to make quarterly payments of $1.4 million until then, where it will probably be re-financed again. The debt is under control with NTELOS’s net debt leverage of 3.6x if using estimated 2015 EBITDA and needs to stay below 4.5x.

The company has extended an agreement with Sprint to be the exclusive wholesale network provider through December 2012, which should bring about $140m to $144m in revenues in 2015. NTELOS is monetizing non-core and underutilized assets such as tower sales and spectrum sale in the Eastern Markets. It’s working on becoming more efficient through reducing cost and corporate restructuring. NTELOS is continuing to roll out the 4G/LTE network with 44% of the POPs covered. The company plans to increase that to 65 percent of POPs covered with LTE by year-end, and expects to complete its LTE network by late 2016 or early 2017. It’s notable that NTELOS doesn’t have a declining legacy business of wirelines.

I don’t expect significant free cash flow for 2015 and 2016 since the capex associated with the 4G network is eating most of the cash flow. It’s in 2017 and the following years that it will get interesting. NTELOS said that about 15% of the capex is maintenance. With $100m in expected capex in 2015, that would mean $15M is maintenance spending. Let’s assume a conservative scenario that in 2018 operating cash flow is ~$100m and capex is $40m, double maintenance rate and more. After debt payment and other expenses, let’s assume there’s $40m left in free cash flow, well that’s almost 40% of today’s market cap. Even with lower operating cash and slightly higher capex, NTLS will be able to grow their equity. I estimate that most of that cash would go to deleverage the company but capital allocation decisions are left to Quadrangle Capital Partners (QCP), the largest shareholder with almost 20% of NTLS. Simple debt reduction could increase shareholder value.

With a market capitalization of ~$105 million, the market doesn’t attribute any value to the restructuring and refocusing effort. NTELOS is making progress towards a leaner more results oriented focused company (instead of fighting the giants for market share in the Eastern Markets). The market also doesn’t attribute any value to a potential takeover offer, which NTLS is occasionally subject to since the industry is consolidating. You eat others or you get eaten. Well NTELOS can’t eat others and it looks good on the buffet table.

The current stock price offers a nice opportunity to get with limited downside. NTELOS is worth something and it’s not the garbage bin price it’s trading at now. I am not pitching the idea that NTELOS will bounce back to the glory days of when it was trading at $35 a share. My analysis is based on an adjustment in the market multiple applied to NTELOS and on what a company would pay for the whole business. We had some indication of value with the rumor that Shenandoah Telecommunications (NASDAQ:SHEN) put together a $200m offer for NTLS at $9.25 per share. This gives you a good idea of what a company would be willing to pay for NTELOS.

At today’s price, this would represent a 94.7% gain compared to the current share price of $4.75. NTELOS is currently trading at about 4.5x (midpoint) projected adjusted 2015 EBITDA of $100 million. Its peers are trading at 7.8x EV/EBITDA. I don’t think NTELOS deserves the same market multiple because 1) it’s smaller and 2) its high leverage restricts operational flexibility. A simple adjustment in multiple to 5x EBITDA would lead to a 30% gain. There are more details on my valuation below.

I expect the results for the next couple of quarters to be messy and not representative as they are winding down their operations in the Eastern Market and refocusing the company. There are costs attached to that (~$50m) and a lot of one-time expenses. However, NTELOS does report the Western Market results separately so you can have a clearer picture of what the company will look like. I expect results in FY2016 to normalize since FY2015 is a transition year with a lot of kitchen sink quarters.

Brief Description of NTELOS Holdings

Feel free to check out the rest of the article here.

Source:

Source: Source: Valener

Source: Valener Source: VNR/Gaz Métro 2014 AIF

Source: VNR/Gaz Métro 2014 AIF Source: BMO Capital Markets – 12th Annual Infrastructure & Utilities Conference

Source: BMO Capital Markets – 12th Annual Infrastructure & Utilities Conference