You have brains in your head. You have feet in your shoes. You can steer yourself any direction you choose. You’re on your own. And you know what you know. And YOU are the one who’ll decide where to go…

– Dr. Seuss

You have brains in your head. You have feet in your shoes. You can steer yourself any direction you choose. You’re on your own. And you know what you know. And YOU are the one who’ll decide where to go…

– Dr. Seuss

This is an update on the restaurant group MTY Food Group Inc. My original article was published in December 2013, so an update won’t hurt. I’ve been more conservative with my valuation. I didn’t include any acquisitions or potential expansion plan in the U.S. If any of the two events happens then MTY is worth more than my estimates. I valued MTY on its current business and not its potential. MTY is a serial acquirer and the market is not giving any value to a potential large accretive acquisition. MTY’s growth-by-acquisition strategy makes it difficult to forecast earnings and therefore to value.

Below is a portion of the article. The full article is available at Seeking Alpha.

TSX: MTY

U.S./OTC: OTC:OTC:MTYFF

MTY Food Group Inc. is primarily traded on the Toronto Stock Exchange under the sticker MTY.

Note: Dollar amounts are in Canadian $ unless mentioned otherwise. USD-CAD 1.3183 Price of 1 USD in CAD as of September 15, 2015.

MTY Food Group Inc. (NYSEARCA:MTY) is a restaurant stock that owns a collection of 35+ brands that operates over 2,792 locations. When you buy MTY, you’re not investing in the restaurants directly. Rather, you’re buying into a royalty stream based on a percentage of the restaurants’ sales and much more. For each plate that is sold MTY earns royalties. MTY simply collects royalties and has very low capital expenditures and financial risk. Because of this successful recipe, MTY receives recurring revenues that contributes to its growing war chest aimed at acquisitions.

Canadians In December 2013 I published my initial research on MTY, MTY Food Group Inc. – A Restaurant Stock For The Wallet. At the time of the publication MTY was trading at $32.75 and has been up and down since then to end up around ~$31 at the time of this writing. If I had published my update just over month ago it would have looked like a winner when MTY peaked to $37.42 on July 31, 2015. Since then MTY has fallen sharply with market turbulence that followed. There wasn’t any bad news linked to the slump in the stock price and just like many companies MTY is simply a victim of the general selloff in global markets.(click to enlarge) Source: Google Finance

Source: Google Finance

However the current drop doesn’t affect the intrinsic value of MTY. The latest price slide offers investors an opportunity to buy it cheaper than when I published my original research. The price per share is cheaper and on a valuation metric basis it’s cheaper too (MTY has grown into its multiple). Expect sharp ups and downs with this stock. MTY is a small Canadian company with rarely any announcements other than results four times a year and the occasional acquisition. Let’s just say that public relation is not their thing. So there are days where you scratch your head when the stock suddenly drops or pops.

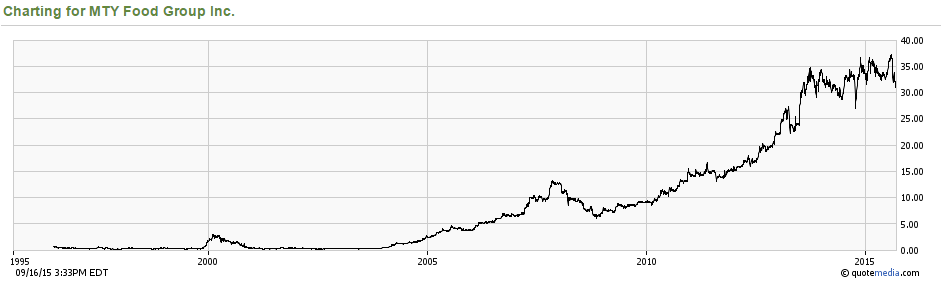

My almost two-year chart above is not representative of the growth MTY had in the past. The chart below represents the compounding effect of MTY. (click to enlarge) Source: Quotemedia.com. Google Finance and Yahoo! Finance only provides graph that debuted once MTY got listed on the TSX. MTY was upgraded to the TSX in May 2010.

Source: Quotemedia.com. Google Finance and Yahoo! Finance only provides graph that debuted once MTY got listed on the TSX. MTY was upgraded to the TSX in May 2010.

The stock really started taking off once it dropped its other business line in 2003 to focus on the food industry. The early form of MTY was in the restauration business but also in IT and other things. That didn’t go well with the tech bubble crash. That’s not the case anymore. Today MTY is much more focused and profitable.

Let’s review why MTY Food Group Inc. is an interesting investment.

MTY Food Group carries a lot of the qualities I look for when investing in a company. The company is easy to understand and franchising is an asset light business model. The business model helped MTY achieve a long history of profitability and generates growing free cash flow. That money is reinvested to compound shareholder value. MTY is headed by Stanley Ma, an excellent capital allocator. He’s disciplined and doesn’t like to overpay for acquisitions. He has proven to be a great steward of shareholder capital. He’s not afraid to say “no” and to walk away if the terms are not satisfying. MTY has also initiated a small dividend in 2010 that’s been growing modestly (well, it has doubled since from $0.05 to $0.10 per share, it represents a 1.27% dividend yield). And more importantly, MTY’s valuation is below its peers. I have a section on the valuation towards the end of the article. Patient investors should realize the benefits of compounding.

There’s no doubt that the restaurant/food industry is hyper competitive. It’s a crazy business to be in. Barriers to entry are low and a successful concept is easily copied. However I believe MTY might have an economic moat. I think MTY has one and it is its concentrated presence in food courts. Aside from Mcdonald’s, Subway, and A&W Restaurant, MTY almost runs a monopoly in most food courts. MTY’s brands are everywhere in the food court. In a food court there are only so many spots available and MTY is the biggest player. I don’t know the exact percentage of MTY’s market share of the food court units, but my personal observations tells me its pretty high. That’s why Stanley Ma has been nicknamed “the king of food court”. Such a concentration doesn’t represent a risk for shareholders. If anything, the recurring revenues from the mall helps finance its expansion on the street front. In Canada MTY might not have the same growth rate as in the past, that’s why it’s turning to the U.S. market for its next growth phase. Consumers looking for a bite at the mall are forced to choose between McDonald’s and MTY’s group of brands. If a location is doing poorly MTY can replace it with another concept. Malls love MTY because it’s only one person/entity to deal with and they will fill up the food court without worrying about if rent is going to be paid on time. You can argue that it’s a form of cannibalization between franchisees but for MTY it still gets its ~6% royalty no matter where the consumer buys its plate. On the downside the mall locations are open fewer hours than the street units. Conversely, the economic moat I’m talking about is not applicable to MTY’s street locations, where it’s really hard to have a competitive advantage for any kind of retailer but you have longer hours. Most of MTY’s units are in the food court but the company has been expanding outside and has been acquiring full service restaurants such as Madisons New York Grill & Bar (great restaurants and ribs by the way, make sure you get a sub-zero pint in a chilled glass)

MTY’s main growth driver is acquisition. MTY Food Group Inc. is a business built on acquisitions. A disciplined approach to acquisition and an under-levered balance sheet (Net Debt/EBITDA 0.27x vs peers 1.5x-1.8x) provides the muscle for MTY to continue their serial acquisition approach. MTY is also looking at the United-States for their next phase of growth where it presently has a small base of restaurants.

My valuation, which is detailed in the article below, only values MTY at its present state. I believe that MTY can deliver a 10-20% return in the short-term. This doesn’t include any acquisition. A growth-by-acquisition strategy makes it difficult to forecast earnings and therefore to value.

Recent acquisitions since my last article are: Madisons New York Grill & Bar($12.9m for 90%), Van Houtte Café Bistros ($950k), Café Depôt, Muffin Plus,Sushiman and Fabrika ($13.9m), Manchu Wok, Wasabi Grill & Noodle and SenseAsian ($7.9m), and most recently MTY will soon be adding Big Smoke Burger ($3m for 60%) to its collection of brands.

If you are an American you probably never heard of MTY and Canadians consume their products on a regular basis without ever knowing it. If you are not very familiar with MTY it’s because you are not going to find a restaurant with the name MTY on it.

MTY operates over 2,792 locations under a collection of 35+ brands. Canadians are probably more familiar with names such as Country Style, Tutti Fruitti, Mr. Sub, Thai Express, Jugo Juice, Cultures, Valentine, Extreme-Pita, or Tiki-Ming, Van Houtte, Madisons New York Grill & Bar, Mucho Burrito, Café Depôt, Manchu Wok, Big Smoke Burger ; all brands that MTY operates. As for the American market, in May 2013 MTY announced their first foray into the U.S. with the acquisition of Mucho Burrito, Extreme Pita and PurBlendz brands. They have every type of chain you can imagine, from sushi to Greek to burgers, with most of the locations in mall food courts. MTY’s current market share is difficult to estimate, due to the continued addition of concepts and the constantly changing competitive landscape. According to Technomic, MTY’s portfolio of brands contains 11 of the top 100 Canadian Restaurant Brands (but I’m usually skeptical of these kinds of surveys). (click to enlarge) Source: AIF 2014. The chart is missing Big Smoke Burger.

Source: AIF 2014. The chart is missing Big Smoke Burger.

When you buy MTY, you’re not investing in the restaurants directly. Rather, you’re buying into a royalty stream based on a percentage of the restaurants’ sales and much more. For each plate that is sold MTY earns royalties. MTY simply collects royalties and has very low capital expenditures and financial risk. The math is simple; more franchises => more sales =>more royalties. Because of this successful recipe, MTY receives recurring revenues that contributes to its growing war chest aimed at acquisitions.

Of the brands above some were developed internally and the rest is from acquisitions and licensing deals. MTY holds the license agreement for Yogen Fruz, Taco Time, TCBY, and Greek restaurant Au Vieux Duluth. For a complete list of the brands (new and old) I would refer you to page 12 of the 2014 Annual Information Report.

The MTY headquarters is located near a major mall in Montreal (Place Vertu Mall). There’s nothing particular about this mall except it’s worth mentioning that MTY maintains a good relationship with the owner of the Place Vertu Mall and the food court there serves as MTY’s personal laboratory. The owner of the mall allows MTY to test new food concepts. MTY owns the lease, so if a banner doesn’t work out it can easily be replaced with a different one. Food courts are great for new brands with little recognition; customers take their tray based on taste impulse rather than brand loyalty. In food courts big bright colorful menus is more effective than traditional advertising. MTY’s multiple banners allow it to have a direct pulse on the trends in the food industry. They have a strong sense for changing public tastes. It also allows MTY to match the cuisine to each location and demographic.

The full article is available at Seeking Alpha.

CAN BOXING TRUST USADA?

QUESTIONS SURROUND DRUG TESTING FOR MAYWEATHER-PACQUIAO AND OTHER BOUTS

By Thomas Hauser (Thanks to Jean-François Corbet from Mount-Royal soccer for the link)

Floyd Mayweather: 48-0* (49-0* next week)

This is the best piece of investigative sport journalism I read in a long time. It’s long article to read and very interesting (more of those are needed). The author leaves no stone unturned. The timing of the article is questionable since Floyd is fighting this weekend. I bet they knew months ago but could get more attention during the media week leading up to a fight. I’m not sure how much leg this article has, but it definitely puts Mayweather on the defensive. It also cast the USADA in a bad light. That group has lost all credibility in the PED/doping/drug world. This article maybe found the next big doping scandal or the whole thing will be throw under the rug. But at the moment of writing these lines it definitely left a mark.

You can probably sense that I’m quick to jumping to conclusion on this only after reading a blog article. Like this blog I can write anything I want. But that piece is so well researched that it’s hard to deny. Unfortunately Mayweather is guilty until proven otherwise. But the guy is allowed a defense. Maybe Mayweather fought clean and the whole thing misunderstanding. However here is what you can’t denied: When you hear about any kind of shady behavior regarding the allegations, it smells bad and it’s doesn’t look good. It’s appropriate that we get to the bottom of this and there should be an investigation. Meanwhile USADA should be denied any Federal funding until this mess is clean.

Questions: Why did Mayweather used an IV before the fight against Pacquiao? And why did he need so much fluid? (an IV helps re-hydrate an athlete but it also helps mask other banned substances.) Mayweather never had trouble making weight and dehydration was never an issue if you followed his career. There are also rumors that he failed drug testing tests in the past but because of special clauses and exemptions to his contract it never became an issue. It’s worth reading the whole thing. At the moment the Mayweather camp is denying any wrongdoing.

Mark Grant, who is a Managing Director of Southwest Securities and one of the most colorful writers on the Greek recurring bailouts, captures the essence of what the bailout really means with this anecdote.

“It is a slow day in a little Greek Village. The rain is beating down and the streets are deserted. Times are tough, everybody is in debt, and everybody lives on credit. On this particular day a rich German tourist is driving through the village, stops at the local hotel and lays a €100 note on the desk, telling the hotel owner he wants to inspect the rooms upstairs in order to pick one to spend the night. The owner gives him some keys and, as soon as the visitor has walked upstairs, the hotelier grabs the €100 note and runs next door to pay his debt to the butcher. The butcher takes the €100 note and runs down the street to repay his debt to the pig farmer. The pig farmer takes the €100 note and heads off to pay his bill at the supplier of feed and fuel. 3 The guy at the Farmers’ Co-op takes the €100 note and runs to pay his drinks bill at the taverna. The publican (tavern manager) slips the money along to the local lady of the night drinking at the bar, who has also been facing hard times and has had to offer him “services” on credit. The hooker then rushes to the hotel and pays off her room bill to the hotel owner with the €100 note. The hotel proprietor then places the €100 note back on the counter so the rich traveler will not suspect anything. At that moment the traveler comes down the stairs, picks up the €100 note, states that the rooms are not satisfactory, pockets the money, and leaves town. No one produced anything. No one earned anything. However, the whole village is now out of debt and looking to the future with a lot more optimism. And that, Ladies and Gentlemen, is how any new Greek bailout package is likely to work.”

Source: Chou Funds Semi Annual Letter

Alan Adler, inventor of the Aerobie Flying Disc and the AeroPress coffee maker, tells the stories behind his famous inventions. This is a short 6 minute video. I received an Areopress as a gift and it’s the perfect machine to make one cup of coffee (Thanks Hugh Langis). The package comes with a lot of tiny accessories but you only really need three things to make the coffee, so it’s less overwhelming than it looks. It also comes with the thinnest paper filter I’ve ever seen. If you look at it on Amazon, it has over 4,000 reviews with an average of 4.6 stars out of five.

Alan Adler, inventor of the Aerobie Flying Disc and the AeroPress coffee maker, tells the stories behind his famous inventions. This is a short 6 minute video. I received an Areopress as a gift and it’s the perfect machine to make one cup of coffee (Thanks Hugh Langis). The package comes with a lot of tiny accessories but you only really need three things to make the coffee, so it’s less overwhelming than it looks. It also comes with the thinnest paper filter I’ve ever seen. If you look at it on Amazon, it has over 4,000 reviews with an average of 4.6 stars out of five.

The following repost is a very detailed analysis of the migrant/refugee crisis in Europe.

Repost From Quinn Diplomacy

By Derek Quinn

Conflict, dictatorships, instability and religious extremism in the Middle East, in the Horn of Africa, and in Central Africa plus the siren call of a better life has resulted in Europe’s worst immigration crisis since the Second World War. Hundreds of thousands of desperate people continue to crowd onto unseaworthy boats in hopes of crossing the Mediterranean, while thousands of Syrian refugees stream along railway tracks in the Balkans in hopes of finding asylum in Europe.

Full article here.

Dow Friday August 21st: 16,459

Dow Friday August 28th: 16,643

Performance: +1%

Last week was some of the five craziest trading days ever. Just by reading the news headline you would have thought the whole world was falling apart again. But guess what, the market closed a little higher (yea). Your portfolio might be flat, but your brain and emotions just got beat up. Imagine if you happened to be on vacation that week, you would have thought that not much happened in your absence. You would have thought “oh, Dow was slightly up 1%, just another normal week, looks like nothing exciting happen”.

These roller-coaster ups and downs can really take a toll on you. Managing the mental ups and downs is more important than trying to manage the market’s ups and downs for most investors. Above average volatility is emotionally taxing. What you don’t want is permanent capital impairment. Permanent capital impairment, not volatility, is the big risk in investing. Volatility isn’t risk unless you have a short time horizon. I believe as long you can ride out the waves, and that your valuation assessment is conservative, then you should do fine in the long run. I recently wrote an article, Keep Calm and Carry On, that provides a reminder in turbulent times.

I’m often asked the question “what do I think about X (oil, Ukraine, China, interest rates etc…)” I can talk about oil all day long but it’s totally different if you are going to go out and invest you hard earned money. Below is my answer.

Question: I’d be really interested to know what you think about oil. There are some very beaten down names…. What’s the strategy here? Is this an opportunity for a long term buy and hold play, or is the consensus that there’s more carnage to come?

Answer: Hi Hank (may or may not be his real name to protect askers identity),

Thanks for reaching out. I follow the oil sector in a general sense but I’m not going to pretend that I’m an oil guru. I’m also not a fan of cyclical investments, such as commodities. You can make a lot of money in that sector but it’s just not my game. You only need to look at the last year or so to see how rock “n” roll prices can be. You can make money really fast and you can lose it even faster. Having said that, I always look for opportunities. Oil is probably the most important and strategic resource we have. Oil’s influence plays a central role in our everyday economy and lives. Regarding oil as an investment, I think I can answer that question in two parts. The first part is your own personal view on oil and the second part is the investment merit of the oil & gas companies.

It’s very difficult to determine the value of a barrel of oil, or any commodity such as gold because you don’t have a cash flow. At least with securities you have a framework for valuing things. For example, a bond is easy to value because it distributes a fixed cash coupon. An ounce of gold just sits there or on a finger. Oil at least has a functional value to society (In gold’s defence, if you watch reruns of Glenn Beck’s show it’s never worth enough). So how much is a barrel of oil worth? I have no idea. Non-income producing assets are worth what buyers will pay for them. For a while the cost of production was a reference for the lowest price possible for a commodity but now we are seeing producers below cost (including some gold producers). One of the main reasons why there are so many companies producing oil below cost or at break-even is because they have to service their debt. It’s pretty much the bank telling them to pump oil because the bank doesn’t care about the economics or fundamentals of oil. As a piece of advice, I would ignore talking heads’ price target on oil. It’s too easy to get sucked in by the fancy sophisticated analysis. The thing is if you listen enough there are so many contradictory targets. Before the oil crash Goldman Sachs was saying oil was going north of $150. Then they changed their mind to $48 a barrel after the crash. You hear so many different numbers being thrown around. What’s insane is that all these analysts have access to the same data bank as everybody else. Basically it’s all noise and those price targets go up and down like the tide. To answer a part of your question regarding if there is more carnage to come, well my answer is how long we will continue to see a decline in the price of oil is anyone’s guess. You really need to develop your own independent opinion with minimal advisory input.

My personal view on oil is that it’s bound to go up eventually. My opinion is not scientifically researched and I don’t have eye popping charts to show you. I also don’t subscribe to any conspiracy theories. My view on oil is simple and easy to defend. You could probably find the same view out of a 6th grader school notebook. In the short-term it’s impossible to know if the barrel of oil is going to $80 or $20. I heard intelligent cases for both side. If your idea of investing in oil is speculating on the price of oil in the next months or years, good luck. I can’t help with that and anybody pretending to is taking you for a ride. If your idea of investing is finding companies or assets trading below its perceived intrinsic value then I can steer you in the right direction.

My case for higher oil is a simple one. Now remember that it’s just an opinion. Demand worldwide should grow modestly over the next couple years. As a society, we still have a lot of work to do before we can switch to a reliable alternative energy source. Basically, what I’m saying is that we are not getting off our oil addiction anytime soon. I love clean energy and it’s definitely the way to go but I’m not giving up my pickup truck anytime soon for a bicycle (However I heard a company called Tesla is up to pretty amazing things with cars).

I do think that low prices is the cure low prices. The lower the price, the higher the oil consumption. (You can also make the case that higher prices is responsible for lower prices) On the supply side, producers just can’t keep operating at a loss forever. According to the IEA, supply will outstrip demand by 2m barrel per day (bpd) for the rest of 2015 and should equilibrate sometime in 2016. It sounds like a lot but it’s not. During Q2-2015, demand was at ~93.5m bpd and supply is at ~96m bpd but some analysts believe the demand side number will be revised upward with demand for gasoline stronger than expected. According to the Federal Highway Administration, the number of miles travelled on U.S roadways rose to the highest level ever in June. It’s easy to disrupt supply. War, geopolitics, a break down in the infrastructure, a problem at a refinery or with a pipeline, issue with transportations are just a fraction of the potential problems that could disrupt supply. Any problem with supply would therefore result in a rapid draw down of oil inventories. Plus you have millions of barrels that need to be replaced every year just because of depletion. Low prices also impact the economics of drilling, reducing additions to supply. What we are seeing right now is that producers are cutting production or leaving oil in the ground. So there’s a lot of pressure on supply. There’s obviously a lot more to oil than what I just mentioned. If you want to learn more about oil I suggest reading letters by Andrew Hall from Astenbeck Capital. That guy knows his stuff but keep in mind he’s a huge oil bull. A good resource is the IEA Oil Market Report. The U.S. Energy Information Administration also post weekly data on oil and energy.

Just being bullish on oil shouldn’t be a reason alone to go all in and invest. Yes there are a lot of beaten up names out there and it looks very tempting to snap a couple shares here and there. The first thing I do is that I go right to the financial statements and start asking questions. Is the balance sheet strong enough for them to survive? Do they have enough cash to meet their debt obligations? In the crappiest environment, how long can they survive? What are the debt covenants? What’s their netback? How much capex do they need and how are they going to fund it? Any shareholder dilution? How long does it take to convert capital to cash flow? Do the math and invest for the maximum risked return.

Depending on how much time you have and knowledge you can poke at different part of the capital structure of a particular company. Distressed debt can be an interesting segment to look at. I would also look for companies that take advantage of the drop in oil price to review their cost structure. For some O&G companies, a drop in commodity prices can be a constructive county cyclical investment strategy which is designed to take advantage of lower activity level and lower service costs to deliver higher returns on invested capital. It’s an opportunity to lock-in suffering service providers at a lower cost. Basically low prices 1) helps weed out the strong ones from the weak ones and 2) and provide an opportunity for companies to plant the seeds of the future if oil prices turn bullish. If they can operate profitably in such a disastrous environment, the rest is upside.

While the upstream (exploration and extraction) side of part of the industry is in pain, the downstream industry which includes pipelines and trains that transport oil is making a killing in this low price environment. As an example, Phillips 66 (NYSE:PSX) and Valero Energy (NYSE:VLO) are pure refiners. As oil dropped, refiners and retailers are acquiring oil on the cheap which leads to margin expansion.

Integrated O&G companies definitely deserve to be looked at. These companies are involved in many aspects of the oil industry, such as upstream, midstream, and downstream. Companies like Exxon-Mobil (NYSE:XOM) and Suncor Energy (NYSE:SU) have their hands in exploration, refining, and retailing. With an integrated oil company, the business is not overly reliant on the price of oil. What they lose in the upstream part of the business, they make up in the downstream sector, so long as gasoline prices stay high.

You can also look at companies that have zero commodity exposure. Usually these companies have a fee based revenue, like pipelines. Kinder Morgan (NYSE:KMI) and TransCanada (NYSE:TRP) are among the companies that operate oil transportation infrastructure. These companies usually have exposure to volume, not price. What they charge is largely independent of oil prices and they are utility like.

If I can resume all of that, I have no clue what oil is worth and what is going to happen. I suggest you develop your own independent opinion. Take a long-term approach and ignore the noise. Wall-Street is not your buddy, pal, friend, or advisor. Basically don’t invest solely on what I just wrote or others. Don’t just snap up shares just because the sector is beaten up. Take a rational, analytical approach to all decisions. Always do the math and invest for the maximum risked return. Act like a crocodile, wait patiently for the right opportunities and take bold action when the time is right.