I’m been trying to make sense of the U.S.-China escalating tension. I believe we are in a cold war. It’s been brewing in the dark for years, each player placing their pieces, trying to get optimal positioning once it breaks out. The cold war is being fought on many front. There’s a trade war, a tech war, an economic war, a covid war, a political system war, and there’s the Hong Kong issue (and Taiwan). Washington is considering a range of sanctions against Chinese officials and firms as punishment for Beijing’s crackdown on Hong Kong. The world is being forced to choose between the U.S. or China, just like the world had to choose between the Soviet Union or America. The list of issues is long. Often, for an successful oversea company trying to growth, going to the NYSE or Nasdaq would make sense.

I’m trying to assess the U.S. threat to delist Chinese stocks. Are they dumb crazy? Is it just politics? Or does it make sense?

Over the years, American investors have been pumping billions of dollars into Chinese firms listed in the U.S., from giants like Alibaba (BABA) and Baidu (BIDU). Investors have been able to profit from the explosion of e-commerce in China, even though the likes of Facebook and Amazon.com Inc. are largely shut out of China.

Recent admissions of accounting fraud at Luckin Coffee have prompted heightened scrutiny of U.S.-listed Chinese companies.

There’s a threat to evict some 170 Chinese companies listed in the U.S.

The move is more than just political. China, uniquely among major world economies, bars the U.S. Public Company Accounting Oversight Board (PCAOB), from monitoring corporate audits, considering that a national-security risk. Chinese audits are done on a completely different basis.

The Senate passed a bill giving all Chinese companies three years to let the PCAOB in, or be kicked out of U.S. markets. It will likely clear the House.

Rumblings about China companies not playing by the same rules have been around for years. The bill will force Chinese companies to abide by the same accounting rules as U.S. companies listed on the NYSE and Nasdaq.

The bill will also require public companies in the U.S. to disclose whether they are owned or controlled by a foreign government, including China’s communist government.

China declares states secrets in not allowing full transparency of corporate books, especially those with heavy state involvement.

Why close the books? Probably what they find won’t be pretty. Opening corporate records could reveal embarrassing links between the nation’s leaders and valuable share packets. Stuff that they don’t want to come out.

The question now is whether we will see Chinese companies give in to the new rules or relocate outside the U.S.

Two of China’s most valuable U.S.-listed companies, NetEase (NTES) and JD.com (JD) are pushing ahead with multibillion-dollar share sales in Hong Kong.

Chinese stock can thrive without a primary U.S. listing, look at Tencent. If you have a good company, you will likely find capital.

Despite the issues with Chinese companies, attracting capital is one of the U.S.’s major force. It’s very important that they keep that advantage. I bet London and Singapore is looking for take advantage of the dispute.

The U.S. instead should have policies to attract listings and capital. One idea is hiring high quality annually-inspected US audit firms.

Companies with good oversights and financial control would probably trade at a premium. Investors prefer companies that have oversight.

It’s important for any company to play by the rule. I don’t think the idea of crippling Chinese capitalism by denying it a listing will work. It’s probably good domestic political firework, but it won’t amount to much. It will probably hurt the country by pushing companies to look elsewhere.

Despite the issues, the U.S. and China should work out their problems. It’s what’s best for everyone’s interest. They need each other. They depend on each other.

China should play by the same rules as everyone. The U.S. should go back to the principles of what made them great.

Get each country’s top three negotiators and send them on an island to work it out behind doors.

I was stuck at home for sixty days with wife and kids. During that time I took on projects that I wouldn’t normally have the time for, such as making maple syrup, brewing beer, making pasta, and baking bread.

I boiled maple syrup because I have maple trees. Made just over 4 liters of syrup. The last 2.5 liters took 30 hours of boiling and used a ton of propane. It was a fun project because I have young kids. They participated at collecting the maple water and sampling various products. This project is seasonal and would have done it Covid or not.

Brewing beer: More of a personal project. I had a beer making kit sitting in the basement and it was about time that I get to it. Kids had fun watching boil the grains and adding hop and stuff. The beer is currently in its second fermentation stage. I will have a taste of the IPA in two week.

Making pasta. The easiest and fastest. And it’s totally family friendly. Fresh pasta is so much better than the box stuff. So much. I don’t know if I can go back. It’s a very underrated activity. The cost benefit ratio is totally tilted towards the benefit. Flour and eggs. That’s all you need.

Baking bread: I joined the sourdough #breadster bandwagon community. I made my starter (5 days) so I can have natural yeast, then another 24 hours for bread making. It’s “labor” intensive. It’s not super physical, but it’s time consuming and you need to be precise with everything. If you are one degree off here and there the whole thing can go awry.

Beer and bread is all about working with yeast and fermentation. With beer sanitation is super important. I got really paranoid with sanitation. Too much bacteria can kill a beer. I learned a lot. Science meets art. Once you master the science and process, you can really start to experiment with several type of grains, hops etc…same goes for bread. The possibilities are endless.

Lessons

I developed a deep sense of appreciation for the miracle of economic specialization. Bread is like $3 and it’s a shit ton of work. I understood specialization as a concept. I understood the benefits, especially when it comes to trade and economic development. But now, anybody that comes up with some protectionist nationalist argument, I would tell them to go make bread.

It’s not breaking news that the energy sector has been a disaster zone this year, as the coronavirus pandemic has decimated global oil demand. There’s an assumption that anyone looking to invest in energy stocks, and oil stocks in particular, is an idiot, and that assumption appears pretty reasonable—if you’re looking in the rear-view mirror. There’s might be better days ahead for the industry. But “when” is the key question. There’s an old saying in the oil industry: The cure to low prices is low prices. I expect more carnage in the short-term before it gets better. Companies will be destroyed. There will be survivors that come out on the other side looking stronger. Their shares are pretty attractive right now. But who will survive? Energy is essential. Although demand is down right now, the world is going to need more energy in the future. Low-cost energy will help to boost the global economy.

But it’s my opinion and I have no money on it, no skin in the game. The sector is too insane for me. It’s driven by too many large actors with non-economic motives (e.g. Saudi-Arabia). Anyway I’ve been reading a lot news of the sector and here are a few insights I picked up. Sometimes in carnage there’s glimmers of hope.

I can’t think of an industry in recent time where even though things could get worse, they got really bad. Predicting a massive drop in oil prices, sure. Predicting negative oil prices? That’s a job losing proposition. Investors in oil have been suffering for a long time.

The market is efficient at pricing in risk. Oil prices have collapsed twice in the past six years. That would tell investors there is a greater likelihood of that happening again. If you’re an operator, this means you might require a higher return than in the past because the risk is greater. If you’re an investor, you require a higher rate of return before you’re willing to invest. Thus, when demand comes back and oil prices recover, the commodity price might be a little higher than it otherwise would have been, depending on how high you need it to be to get that marginal barrel produced.

The world is still highly reliant on hydrocarbons. Renewable-energy sources are growing, but long-term demand for oil and natural gas is growing faster in percentage terms.

The May futures contract for WTI crude turned negative in April (-$37 a barrel), as demand plummeted and storage capacity ran out. That seemed to be an unusual set of circumstances with open futures contracts and perhaps some unsophisticated investors who got stuck. The lesson: Don’t hold financial contracts that you can’t honor as expiration approaches. With limited-to-no storage capacity available at the delivery point for the WTI oil-futures contract on May 19 (Cushing), so holders of financial contracts will need to sell prior to expiration. If open interest remains high as we approach expiration, then negative oil prices are possible again.

Negative oil prices were an anomaly—a function of a timing mismatch between the pace of demand reduction and that of supply reduction.

You need to break down the oil industry in two players: Producers and refiners. In between you have the pipeline, storage, and the infrastructure (mid-streamers). In normal times, good news for producers would tend to be bad or neutral for refiners, because refiners have to buy from the producers.

The hope is that the oil market rebalances and every part of the industry improves — oil and gas producers make more money selling crude, refiners sell more gasoline, and pipelines see more activity.

Refiners have been cutting back on processing crude because there are too few buyers. No one is driving as people stay at home to stop the virus, and gasoline is normally the number one use of crude in the U.S.

U.S. oil prices have jumped 99% in just the past week, an incredible performance that has made energy a top performing sector after months of under performance. Investors bet that companies in the beaten-down sector can come back from a historic rout in the first quarter. Even with the latest surge in stock prices, it should be noted that nearly all energy stocks are down by double-digit percentages for the year. Crude is up for two reasons:

One is that investors now expect demand to return for major products like gasoline and diesel as countries start loosening lockdown orders imposed to stop the spread of the coronavirus.

That oil companies have gotten more serious about reducing supply. U.S. oil production has already declined by almost 1 million barrels a day since it peaked in March, according to Rystad Energy.

The Texas and the U.S. responds to market prices, not government or OPEC. Earnings releases from U.S. oil companies show they’re prepared to make dramatic cuts.

The idea of the Russia-Saudi Arabia price war is to drive U.S. producers out of business. It might work to a certain degree. That playbook employed in 2014 with limited success. Now S-A is trying again with a weaker hand. You might end up with zombie companies like in 2014, where U.S. producers pump just enough to cover interests on the loan.

Mass bankruptcies look unlikely, at least in the short term. And if riskier companies can hold out until oil prices rebound, they are likely to be in a position to produce better cash flow next year. Oil futures a year out are projecting West Texas Intermediate crude at $33.

For companies to produce oil profitably, Brent needs to trade around $50 a barrel. Back in December, with the Brent at $60, companies with the right structure could thrive and cover their dividends fully. Oil companies were buying back stock with excess cash flow. They could compete with the S&P 500 on a cash-flow-yield basis. Today the math doesn’t work at current prices.

I was surprised to learn that energy stocks now account for a measly 3% of the S&P 500 index, thanks to a terrible decade and massive technology companies. It’s much higher than that in Canada. I know it was at least a third of the index at one point but I don’t know if it’s still that high now.

Most oil and gas producers, including the majors, will lose money in 2020 or barely eke out a profit, and most of those still paying dividends will have to borrow to cover the cost.

They key for oil companies is reducing production, slashing costs, and conserving cash. These steps are likely to pay off in higher oil and gas prices over the next two years—and stronger operations and balance sheets for the industry’s survivors.

Royal Dutch Shell Plc. (RDS-A, RDS-B) cut their dividend for the first time since WWII, to 16 cents a quarter from 47 cents for a 66% cut. For a company that seems to want to be around for a long time, it’s the prudent move. Most companies, including Exxon, BP, and Chevron should cut but won’t. Instead they are delaying capital expenditure. You can only do that for so long before it bites you in the butt.

Take Exxon for example. Analysts think that Exxon will generate $2 billion of negative free cash flow this year, with a $15 billion dividend commitment. The company recently issued $18 billion of debt, which could cover this shortfall, but one could definitely question how long it makes sense to do so.

I think Shell is the most anti-oil oil producer. Shell is thinking about the long-term transition away from fossil fuels. Shell leads big oil in the race to invest in clean energy. Shell has this “Sky” scenario plan that highlights the transition toward a clean energy world by 2070. It’s much later than the U.N. 2050 plan and is probably more realistic.

Everybody talks about the negative impact on U.S. producers. That Russia and Saudi Arabia are trying to drive them out of business and that Saudi Arabia wants to regain the crown of world’s largest producer. But there are other major global impacts that won’t go unnoticed. Low prices will hurt or destroy many countries dependent on oil. This can’t be good for enemies of the U.S. that are not under their political and/or military control, such as Venezuela and Iran (also Saudi-Arabia’s rival/enemy). This can’t be good for Russia also but I think they have enough foreign reserves to withstand the storm in the short term.

OPEC++++ agreed to cut production by nearly 10 million barrels a day, starting this month, to help to rebalance the market. I’m very skeptical it will work. First the math doesn’t work. For the near term, it’s too little, too late. The cuts agreed to are starting from a base level in October 2018, when OPEC was producing at a higher level, so the effective cut is more like 7.1 million barrels. Balance and supply is out of whack by way more than 10m a day. Second, if you look who the countries who signed the deal, how many of these countries can you trust? OPEC alone has had time keeping their members from cheating. The whole thing almost fell apart because of Mexico. This is not an easy agreement to implement. Here’s an headline: Iraq faces problems cutting 1 mln bpd of crude output -sources

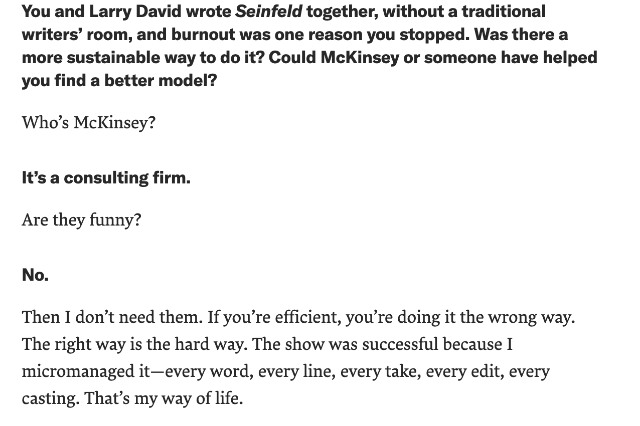

I came across this gem on Twitter. The image below is a snapshot of an interview Harvard Business Review conducted with Jerry Seinfeld in 2017. Two question in and the interviewer brings up the consulting firm McKinsey, well because it’s Harvard. Anyway I though the following exchange was very funny.

There’s a lesson here. The quality of the answers is positively correlated to the quality of the questions. Ask dumb question, get a dumb answer (or a funny in this case).

First, some comments on the pre-AGM webinar hosted by Professor Lawrence Cunningham, then I will comment on Berkshire Hathaway (BRK). Professor Cunningham occasionally does this kind of event and is generous with his time. Here’s the recording.

There were about a thousand of us on Zoom. Professor Cunningham did something similar two weeks ago when for the launch of his new book: Dear Shareholder: The best executive letters from Warren Buffett, Prem Watsa and other great CEOs (see post). Professor Cunningham is a Buffettphile. Lawrence is a professor of law at Georgetown. But he’s better know for his work Buffett and BRK. Lawrence has done a great job representing Buffett’s views. He had access to Warren for over twenty years. He has documented many angles of BRK/Buffett through the years. If you are an investor and you want to get better, then the book you should read The Essays of Warren Buffett: Lessons for Corporate America. A new edition comes out every five years to stay current with Buffett’s views. The book covers a lot of topics. Corporate governance, culture, management, values, investing etc…really it’s a gem. It’s not that big and packs a lot.

Anyway the pre-AGM meeting was good to get into some-kind of BRK groove. I don’t know if you have been to a BRK AGM, but an online AGM doesn’t quite catch the vibe. If you are a value investor, you have to attend at least once in your life. Hopefully we can defeat COVID-19 ASAP and move on to better things.

Berkshire Hathaway Notes

It goes without saying that BRK is a special company. There’s nothing else like it. There are clones, but they are not as successful. Maybe except for Markel Corp. (MKL) which is probably the best clone I can think off. MKL emulates BRK and Buffett in many ways. They have good insurance companies, good management, good businesses, a good culture and a great shareholder letter. Fairfax has solid insurance companies but is lagging behind on the investment side. I don’t know if there’s something equivalent of a BRK in Europe or Asia (there are a lot of giant conglomerates). The BRK recipe has been laid out. You can copy it. But the large majority can’t do it. BRK has such a unique culture which explains why it’s hard to replicate (autonomy, decentralization and trust). Also people don’t have the patience. Everybody wants to be rich but they don’t want to do it slowly.

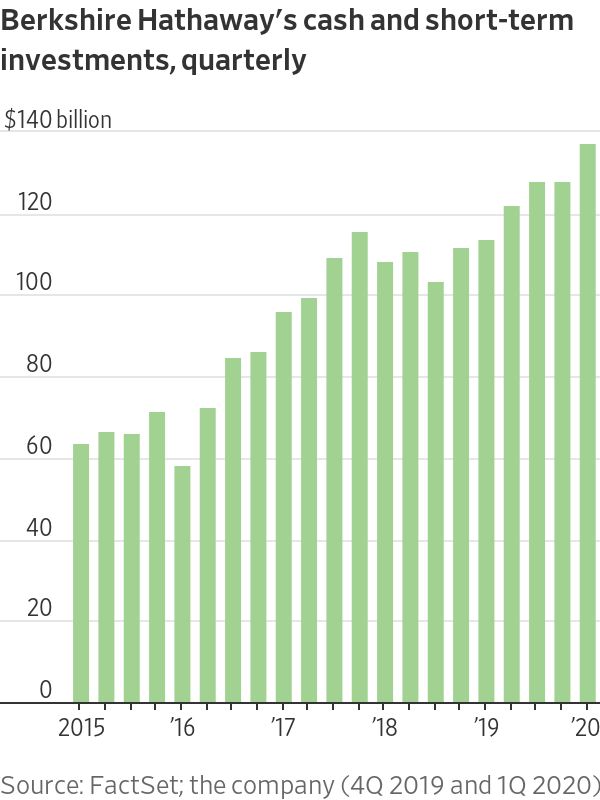

That Cash Pile

BRK is sitting on $137 billion and he’s getting heat for it: “He’s not buying anything, he missed the dip, he didn’t do enough buybacks etc…” So who cares about sixty years of investing greatness. Really I don’t get the hate. I saw a video of a guy on Twitter burying a Buffett book. To the people that are giving Buffett crap for having all that cash, just take a quick look at the state the companies that don’t have any cash are in.

I don’t know about you but that pile of cash looks really good right now. We are a quarter into this Covid-19 mess. There’s a lot we still don’t know. We have no clue how this will play out. A second wave? Another shutdown? An Italian style public health crisis? We will get out of this mess eventually, but when and how much it will cost are unknown (astronomic!) A lot of people pretend to know, but nobody knows.

The current market rebound doesn’t reflect the reality I see right now. People are losing their businesses, their jobs, their savings, debt is pilling up…none of this is a quick fix. I understand that the market is forward looking and that most of the valuation is on the back end (terminal value). We will have a better idea of the real damage done in the summer and fall once bankruptcies starts to flood in. Governments are telling restaurants to open at 50% capacity. Do you know how hard it is to make money with a restaurant running a full capacity during good times? What about these stores in the mall? The current market rebound is based on the central banks doing everything there is to do to at any cost.

Buffett also said this about the $137 billion he had on hand: “Isn’t all that huge when you think about worst-case possibilities.” He’s certainly in a better position than anyone to make that judgement call.

The Fed

Back during the Financial Crisis of 2008-09, BRK made some of the sweetest deals. Buffett saved Goldman Sachs, General Electrics, Bank of America, Harley Davidson, Tiffany and I’m sure they are more. He had money, they needed it.

This time there were no deals. The main reason was the the Federal Reserve and government stepped in very aggressively. They learned from the last crisis. And you can’t compete with their terms.

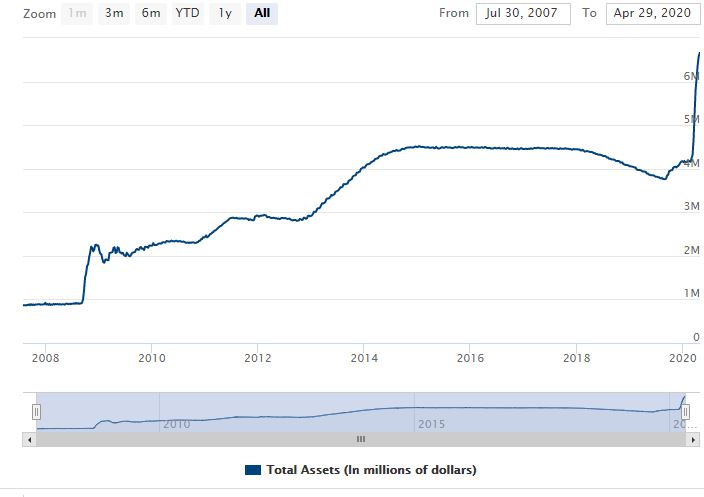

As a consequence of their buying spree of epic proportion, the Federal Reserve’s balance sheet has exploded to over $6 trillion. Look at that spike at the end of the graph. That’s one swollen balance sheet.

Federal Reserve Balance Sheet as of April 29, 2020

Bearish

Six months before the bottom in March

Buffett is known for his eternal optimist. People turn to Buffett for some-kind of hope. Back in 2009 he wrote an op-ed in The New York Times saying he is buying American stocks! Then the market went down for another six months. But his message and action remained iconic. Having the right temperament and attitude can help you navigate hard times.

Last Saturday listeners where waiting for this kind of up-beat mood lifter and let’s just say they got buzz killer. He came across as quite bearish (more realistic IMO) during the virtual meeting and that’s scary. Investors turn to Buffett for guidance during hard time. Stocks are apparently low (kind of not really) and he’s not buying. It’s probably not the message investors wanted to hear. But sometime you need to hear the truth. And right now the truth is not going to be pretty for a while. Remember he’s an Oracle…

You have to understand that through BRK, Buffett has a direct pulse on the business world, from small to big businesses from many different industries. He knows what is going on.

Also when Bill Gates is your best friend, and Bill seems to knows everything there is to know about pandemics and Covid, you are probably getting better facts than the White House briefings.

“I Don’t Know”

Buffett said “I don’t know” a lot during the meeting. Smart people says I don’t know a lot.

I think we don’t say it enough. Buffett understands his circle of competence. If it’s out of his league, than you get a “I don’t know”. It’s important to be intellectually honest. That way we can grow and make less mistakes. We should say “I don’t know” more often. It will prevent less b.s. floating around.

Successor

Nice to see Greg Abel up there. We got an extensive look at a man who could succeed Warren Buffett. He looked good. He demonstrated very broad knowledge across the company. Abel is a vice chairman for non-insurance operations. Abel gave investors a sense of how those operations were adjusting to the coronavirus pandemic and economic landscape. The other candidate for succession, Ajit Jain, is the vice chairman overseeing the insurers.

Buffett Exits Airlines

How to you become a millionaire? You start off as a billionaire then buy an airline.

Buffett sold all his airlines. Good riddance. “When we change our mind, we don’t take half measures”. To Buffett’s credit, he didn’t nor seek to assign blame elsewhere. He just said he made a mistake.

There’s probably other motives too. Buffett is the 2nd or 3rd richest man in the world and ex biggest investor in the airlines. Just think of the headline: “Billionaire Buffett’s Airlines receive bailout money” or “$137 billion cash pile and Buffett needs government help”. Buffett is careful of his image and he doesn’t need that political/public backlash that would have follow. Billionaires don’t need a bailout. He made a mistake, recognized it, and move on.

Quiet Buffett

As the coronavirus crisis unfolds, many are asking: Where is Warren Buffett? They want to hear and see more from the famed investor, noted for both calm and prowess in times of distress. Well he did an one interview back in February (CNBC) and another one in March(Yahoo! Finance). His AGM was coming up so most likely save the spot for all the questions. Buffett has already given the world so much. He’s 90 years old. He’s been doing this for sixty plus years. He doesn’t owe us anything more than he’s already said and done.

It’s possible there are other forces at work here. We are in a pandemic and recession. I’m not sure it’s smart to have Buffett hopping around of happiness like a little kid because “the supermarket is on sale” while people are dying or losing their jobs, money, or business.

It’s not breaking news that the energy sector has been a disaster zone this year, as the coronavirus pandemic has decimated global oil demand. There’s an assumption that anyone looking to invest in energy stocks, and oil stocks in particular, is an idiot, and that assumption appears pretty reasonable—if you’re looking in the rear-view mirror. There’s might be better days ahead for the industry. But “when” is the key question. There’s an old saying in the oil industry: The cure to low prices is low prices. I expect more carnage in the short-term before it gets better. Companies will be destroyed. There will be survivors that come out on the other side looking stronger. Their shares are pretty attractive right now. But who will survive? Energy is essential. Although demand is down right now, the world is going to need more energy in the future. Low-cost energy will help to boost the global economy.

It’s not breaking news that the energy sector has been a disaster zone this year, as the coronavirus pandemic has decimated global oil demand. There’s an assumption that anyone looking to invest in energy stocks, and oil stocks in particular, is an idiot, and that assumption appears pretty reasonable—if you’re looking in the rear-view mirror. There’s might be better days ahead for the industry. But “when” is the key question. There’s an old saying in the oil industry: The cure to low prices is low prices. I expect more carnage in the short-term before it gets better. Companies will be destroyed. There will be survivors that come out on the other side looking stronger. Their shares are pretty attractive right now. But who will survive? Energy is essential. Although demand is down right now, the world is going to need more energy in the future. Low-cost energy will help to boost the global economy.