I didn’t type these notes. They were sent to me. The raw text is from CNBC.com and the personal responsible for the notes compiled them for their own reading. I though the notes were excellent and asked for permission to share.

Charlie Munger spoke to WSJ reporters Nicole Friedman and Jason Zweig for six hours over dinner in his Los Angeles home on April 23. He covered a wide array of subjects. Here is an edited transcript from that conversation and a follow-up telephone discussion.

Q: What do you make of the world-wide fan club that you and Warren Buffett have attracted?

A: Well, the world is very peculiar. And these people that like me are mostly nerds in China or India. It’s a very deep attachment. They’re so passionately interested in improving themselves. Some of them just want to get rich in some easy way, but mostly they’re trying to improve themselves.

An awful lot of graduates of great engineering schools are investors. I wouldn’t call a man who uses computer science to sift vast amounts of data for correlation, and then starts trading the correlation and if it works, keeps going, and if it doesn’t, stops, I wouldn’t call him an investor. It’s really, what he is is a trader. And those correlations are very peculiar…. Of course, the more people that try and trade that one correlation, once they find it, the less well it works.

Q: If you were just starting out as an investor, what approach would you take?

A: Well, the original [Benjamin] Graham approach of looking for cases where you’re getting more than you’re paying for is correct. All good investing involves getting a better investment than you’re paying for. And you’re just looking for it in different places, just as a fisherman can fish in one place or another. But he’s always looking for more value than [he’s] paying for. That will never go out of style. I mean, that is just basic and fundamental.

Some people look at it in stocks where the earnings are going up all the time, some look at consumer goods, some look at bankruptcies, some look at distressed debt. There are different ways to hunt, just like different places to fish. And that’s investing.

And knowing that, of course, one of the tricks is knowing where to fish. Li Lu [of Himalaya Capital Management LLC in Seattle] has made an absolute fortune as an investor using Graham’s training to look for deeper values. But if he had done it any place other than China and Korea, his record wouldn’t be as good. He fished where the fish were. There were a lot of wonderful, strong companies at very cheap prices over there.

Let me give you an example. One guy in Korea, he cornered the sauce market. And when I say cornered, he had like 95% of all the sauce in Korea. And he couldn’t stand anybody else ever selling any sauce. So he could have made two or three times as much if he wanted to by raising the prices.

This post is a little overdue. Better later than never I guess. With the Berkshire Hathaway AGM this weekend, I told myself to get this post done.

Three weeks ago I was in Toronto for the Fairfax Financial AGM (FFH), the Fairfax Africa AGM (FAH.U), and the Fairfax India AGM (FIH.U). That’s the “official” reason. But more importantly and more interestingly are the associated events surround the Fairfax AGM. It’s very similar to what you would find in Omaha for the Berkshire Hathaway AGM, except on a smaller scale. It’s my second time to the Fairfax AGM and I would argue that I prefer that one to the Berkshire AGM. I’m certainly not implying that Fairfax is a better company than BRK because it’s not. I just prefer the Fairfax AGM better but when I think of it, I don’t.

The reality is that I don’t care about Fairfax and its AGM. The reason I go to Toronto is to reconnect with fellow minded investors and the associated events. There are value investing conferences, dinners, and other events like that. Even if the Fairfax AGM didn’t exist I would go only for these events. While I was there I presented at the YYX Toronto Value Symposium, attended The Ben Graham Dinner, and attended the Premier Fairfax Financial Shareholder’s Dinner. There are other events as well such as The Ben Graham Centre’s Value Investing Conference but it conflicted with the the YYX Toronto Value.

Basically you are surrounded by like minded investors and you talk stocks for 2-3 days.

Can We Stop With The “Warren Buffett” Label?

Prem Watsa has been labeled the “Warren Buffett of the North” in the past and I doubt the moniker still holds. Sure they are some similarities. They both run massive conglomerates with insurance powerhouses that invest the float in a bunch of businesses. And the similarities stops there. Fairfax’s returns in the mid-80s and 90s were decent, but have been frustratingly subpar for a long time while Berkshire Hathaway has been outperforming the S&P left and right. People listen to every word coming out of Warren Buffett’s mouth. Every investment article has a Buffett quote. I can’t recall a Prem Watsa quote. I read Fairfax’s shareholder letter. It’s fine if you want to learn more about Fairfax’s businesses but it’s not the source of investment wisdom you would find in a Warren Buffett letter. This post is not a Prem Watsa rant. I might sound overly negative but by labelling Prem “The Buffett of the North”, you are comparing him to the best investor of all time and that’s impossible standard to live up to.

So can we stop with the “next Warren Buffett” moniker. And not just on Prem. The “Warren Buffett” label is like a curse. Look what happened to Bill Ackman and Eddie Lampert. These magazine covers didn’t aged well.

Eddie “The Next Warren Buffett” Lampert and Bill “Back Buffett” Ackman

Prem is Prem and that’s perfectly fine. Nobody else in the world is Warren Buffett. The expectations that come with the label, to put it mildly, are unreasonably high. Buffett has something like 50+ years of over-performance. In today’s hyper-speed era, we don’t have time for a 10-year, or even a 5-year performance table. Now crank you a couple years of decent returns you too can get the “Buffett Crown”. It’s dangerous because investors now expect you to repeat your past performance.

I have three messages: 1) Stop calling an investor on a good run “the next Buffett” and 2) the next time someone’s being lauded as the next Warren Buffett run the other way. History is not on your side. And 3) Warren Buffett is still alive and you can invest with him.

Fairfax’s Investment Portfolio

Fairfax mentions that could have earned a 15% return on equity if their stock portfolio achieved a 7% return and their insurance operations produced a combined ratio of 95%. The insurances companies produced a 97.3% combined ratio and only 3.1% on the stock portolio. Book value was down 1.5% in 2018.

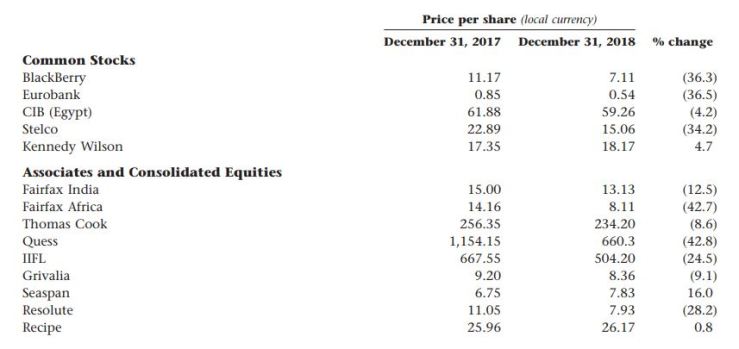

Below is part of Fairfax’s investment portfolio. They have a $39 billion investment portfolio.

Source: Fairfax 2018 Shareholder Letter

I don’t know about this investment portfolio. Part of the uncertainty is that I’m not familiar with some of the companies. The hope is that it will pay out in the long term. It’s definitely different, than let’s say what BRK does with its float. One thing however is that you can’t accused Prem of being an closet indexer.

Blackberry (BB) seems to be turning things around but can Fairfax recuperate the losses from their six year old investment? Blackberry is a good company but the acquisition at the time was terrible timing at a bad price. FFH owns 95 million shares at a net cost of $12.30 per share. I believe Seaspan (SSW), under the leadership of David Sokol, will do fine in the long-term.

I find Prem’s action hard to understand. The macro predictions, shorting the index, the stock portfolio, the underperformance…

“Your Chairman continues to learn – slowly!!” – Prem Watsa

YYX Toronto Value Symposium

This is one of my favorite event to attend. I attended and presented at the YYX Toronto Value Symposium. The event structure is similar to a ValueX conference. You have about 30 people, around 10 people present an investing idea for 15 minutes followed by quick a Q&A. If I have to estimate, half the room were Americans and Canadians.

I think this event delivers a lot of value. You leave with a bunch ideas that you can further research. Most of the stocks pitched are companies I never heard of. Stuff under the radar, not followed, misunderstood etc…If you are an investor, you know how long it takes to find and analyze ideas.

A big thanks to James East for organizing such a great event.

Fairfax India & Africa

Two different funds in two different region. I attended both presentations and they both look promising. Both fund AGM are interesting, better than the parent AGM. They are more detail oriented. You get a walk through of the investments process and the results. I think the best investment they made is the Bangalore Airport in the India fund. That investment has produced great results and I believe it will delivery even better results in the future. The company is not public yet, so if you want exposure you have to buy the India fund or try to get Siemens to sell you their stake.

I’m not an investor in neither fund at the moment. I’m a little uneasy with the structure, the fees, and some of the investments. I also need to do further homework.

Conclusion

I wish I could spend more time talking about the events and companies involved. I could write about this all day but my time is scarce.

To concluce, the Fairfax AGM is not really about Prem or Fairfax. It’s about a bunch of value investors getting together, trying to learn and find new ideas.